Teenhood is the first time children are exposed to financial autonomy; to be a teenager means to be a spender. However, this can also cause reckless spending due to teenagers’ lack of experience with finances. With no formal education on money, many teenagers don’t know how they should be spending their funds.

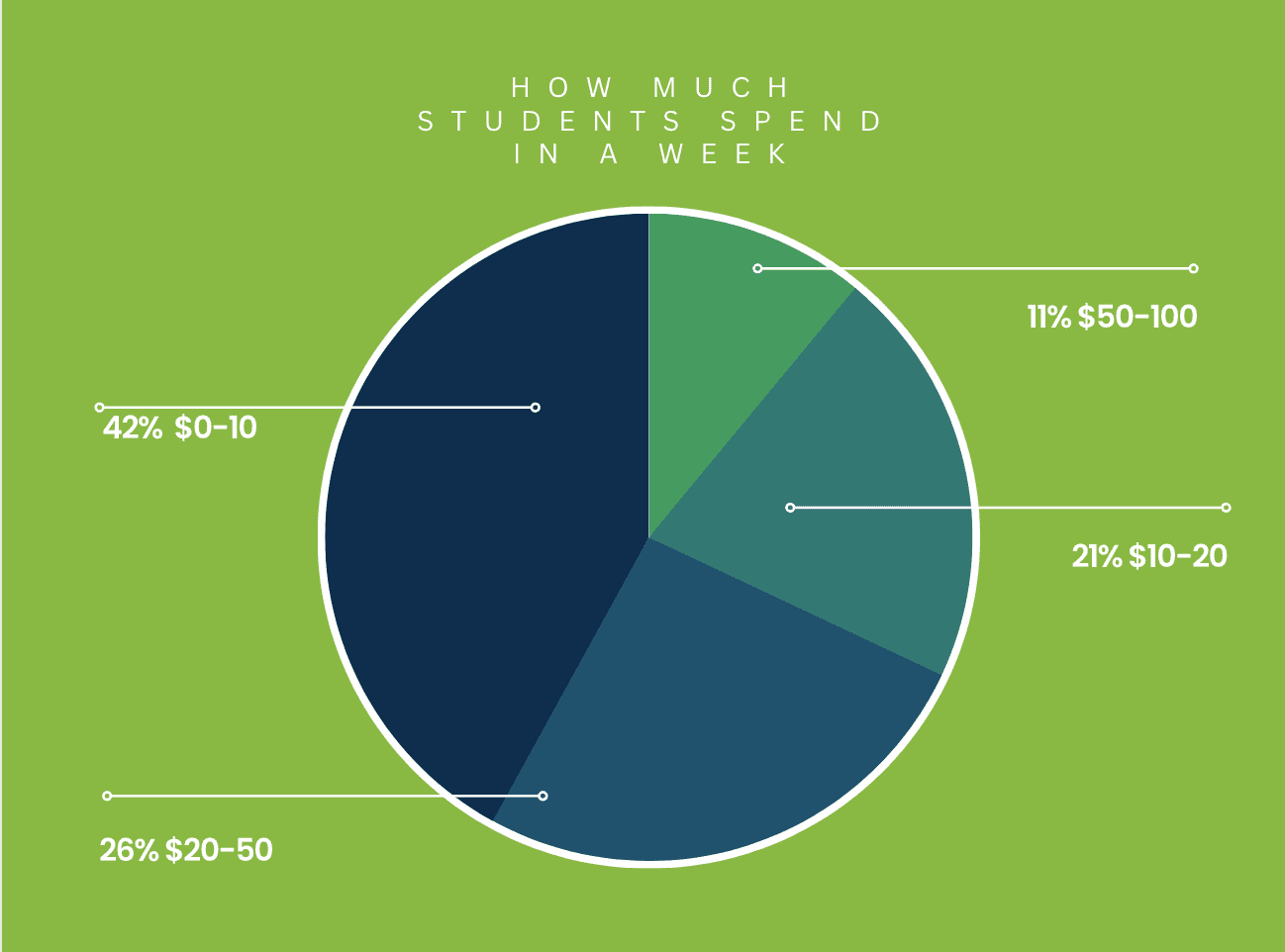

Out of 111 M-A students surveyed, 42% spend $0-10 a week, 26% spend $20-50, 21% spend $10-20, and 11% spend $50-100. A majority said they spend their money on snacks and clothing.

In a different poll, 15 out of 22 students said they would benefit greatly from having a class on finances— many M-A students don’t consider themselves financially literate.

For Economics teacher Stephanie Cuff-Alavarado, long-term thinking is key. She said, “Retirement is something I’ve read a lot about. By the time you’re 24, you want to have about $25,000 saved, but that becomes more challenging due to increasing student debt. Students are graduating with never-before seen debt unless you benefit from generational wealth.”

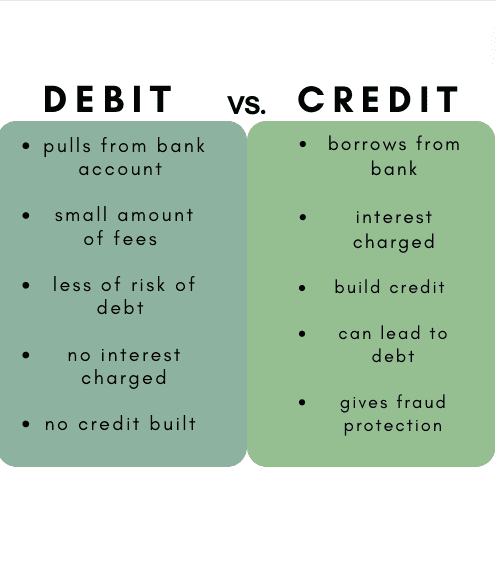

A main facet of thinking ahead financially is not just how you spend your money, but what you spend it with. “Students don’t have a great understanding of planning out long term, and I think that applies to how some folks might approach a debit card,” Cuff-Alavarado said.

A debit card pulls directly from your spending account so you can spend more than you intended very quickly. Cuff-Alvarado pointed this out, saying, “When we swipe, we don’t realize how much money we’re losing. Swiping is so easy, and I’ve seen a lot of students rack up debt very quickly.” If you get a credit card, be very careful. Unlike debit cards which pull directly from your funds, credit cards borrow money by using a line of credit, which you have to pay back later. A study by MIT found that using credit cards activates the reward system in your brain, causing you to seek out more of that feeling. Swiping a card releases endorphins, causing you to want to do it again, and as soon as possible.

When shopping online, the intangibility of money often causes teenagers to overspend. If you’re a teen or a young adult, many large companies— especially fast fashion brands— will take advantage of you. For example, companies like SHEIN trick you into spending too much via alluringly low prices. This is why experts suggest the use of cold hard cash when spending; it helps keep your spending in check as it doesn’t have the illusion of bottomless spending like debt or credit cards. Cuff-Alvarado said, “If you can see what’s in your wallet, you’re more likely to stick to your budget.”

“If you can see what’s in your wallet, you’re more likely to stick to your budget”

If you get a credit card, do your research to ensure you choose a company that offers a lot of rewards. Steer clear of cards offered by retail stores, like Target and Walmart. Cuff-Alvarado said, “Most stores make a large percent of profit on the interest of debt you can’t pay off. This can be predatory and dangerous.” Cuff-Alvarado added that if you do decide to get a card with a store, go with Amazon, as it provides a vast array of products and services.

Be sure to consider using a travel card if you or your family travel frequently. Cuff-Alvarado advised, “Make sure you always pay off the balance—that’s how you make that credit card company work for you instead of you working for the company.”

“Make sure you always pay off the balance—that’s how you make that credit card company work for you instead of you working for the company.”

Another important tip is to create a budget and stick to it. There are many budget templates online that are highly customizable, affordable, or even free. Find one that works for you and use it to better record your spending. This both helps with your understanding and control of your present finances and practice for the future. As an adult, effective budgeting will be instrumental to any form of success, and it’s imperative that you get used to it.

Where you shop can also help with being financially responsible. Cuff-Alvarado strongly advocates for buying second-hand and frequenting thrift stores, giving a shout-out to Savers in Redwood City. According to the same survey, 44% of students said that they don’t go to second-hand stores even though thrifting is an affordable way to get both necessities and luxuries. However, be wary of consignment stores which sometimes overprice their items. Cuff-Alvarado criticized this, saying, “Due to the popularization and even gentrification of thrifting, some people are being priced out—especially those who need it the most. The capitalization of thrifting has made it sort of elitist.”

Finances can be intimidating, and even scary at times. Cuff-Alvarado said, “Oftentimes people can get into financial trouble for not reading or understanding all the terms.” To avoid legal trouble and stay in the loop about your finances, ask questions to workers at the bank and your insurance providers when you don’t understand something. The only way to build up financial literacy is by asking questions. Talk to your parents, teachers, and peers. “Especially teachers,” Cuff-Alvarado said. “Chance is, most of your teachers have been broke at least once.”

M-A does not provide a Financial Literacy class. Cuff-Alvarado maintained that despite the curriculum’s lack of a more specialized class, Economics is the second-best thing. She said, “It’s going to give you the correct vocabulary and explain what’s going on financially in the world around you.” The class contains an important connection to financial literacy, which is advantageous.

These basic tips can help when trying to navigate the world of finances. Cuff-Alvarado is a resource if students are still looking for financial advice. She said, “If anyone wants help, has questions, or wants to start an after-school financial literacy club, ya girl’s available.”